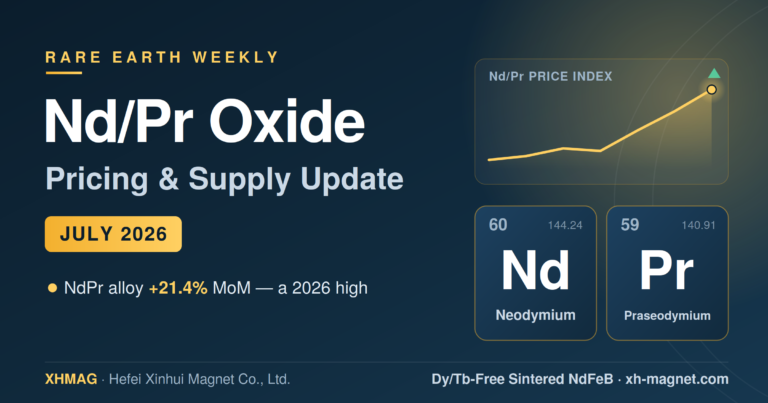

NdPr oxide — the core raw material in every NdFeB magnet — opened 2026 at ~$53/kg, climbed to ~$138/kg by late April, then pulled back to ~$90/kg by June. For anyone sourcing NdFeB magnets, understanding what drove that move — and what comes next — is the difference between a well-timed order and a costly one.

PrNd (praseodymium-neodymium, also written NdPr or PRND) is the blended rare earth oxide that every sintered NdFeB magnet is built from. In a typical magnet it makes up 25–32% of the weight and 50–65% of the material cost — which means when the PrNd price moves sharply, magnet buyers feel it, usually with a lag of one to two quarters.

In 2026, PrNd prices opened the year at ~$53/kg and rose to ~$138/kg by late April — a gain of nearly $85/kg in sixteen weeks — before correcting to around $90/kg by June. That still leaves prices 70% above the year-open. This guide answers the two questions the title asks: what is driving these costs, and what does it mean for your next order.

What PrNd Is — and Why It Drives Your Magnet Price

Praseodymium and neodymium are chemically similar light rare earth elements that occur together in ore and are refined together as a blended oxide — roughly 75–80% Nd and 20–25% Pr by mass. Magnet producers use this blend directly rather than separating the two elements, which reduces processing cost without affecting magnetic performance.

Every kilogram of sintered NdFeB magnet contains approximately 25–32% PrNd by weight. At current oxide prices, that translates to 50–65% of the finished magnet’s raw material cost — more than iron, boron, dysprosium, and coating combined. This is why PrNd price movements pass through to your magnet quote faster and more directly than any other input.

- PrNd oxide — 25–32% by weight, 50–65% of material cost. The dominant variable. When the oxide price moves, your magnet price follows.

- Iron (Fe) — ~65% by weight, ~10–15% of cost. Abundant and cheap; not a meaningful cost driver.

- Dy / Tb (heavy rare earths) — 0.5–5% by weight, 10–30% of cost. Tiny amount, outsized cost impact, especially for high-temperature grades (SH/UH/EH).

- Boron and other additions — under 2% by weight. Minimal cost contribution.

Indicative ranges for standard N35–N52 sintered NdFeB. HREE content varies significantly by grade and operating temperature.

The 2026 Price Story: How We Got Here

The 2026 rally unfolded in two waves, separated by a brief mid-March correction. Understanding the sequence matters: each inflection point reflects a specific trigger, and those triggers have not gone away. The seven milestones below trace the move from $53/kg to $138/kg and back to $90/kg.

Year open; global magnet inventory lean after a quieter 2025; restocking season begins

Northern Rare Earth and Baotou Steel announce Q1 concentrate price hike — bullish signal ignites speculative rally

Rally extends; China Rare Earth Price Index surges; pre-CNY restocking demand accelerates the move

CREA index at 2-year high; heavy rare earths (Dy, Tb) surge simultaneously; Western buyers begin precautionary buying

Chinese magnet makers adopt wait-and-see stance; downstream resistance to elevated prices triggers partial Q1 correction

Second surge: NdPr metal benchmark touches $136–$139/kg — the 2026 high; Western OEM precautionary buying intensifies

~35% correction from April peak; speculative positioning unwinds; still 70% above year-open

What’s Driving the Cost: Five Structural Forces

The price move from January to April was driven by five forces that reinforced each other. None of them have been resolved by the June correction — which is why understanding them is the key to reading whether today’s $90/kg is a buying opportunity or a pause before another leg up.

01China’s mining quota system (MIIT)

The Ministry of Industry and Information Technology sets biannual mining and separation quotas that hard-cap how much PrNd oxide China can produce in a given period. In 2026, quota tightening combined with environmental enforcement at major northern separation facilities critically limited physical availability — even as demand held firm. When Northern Rare Earth raised Q1 concentrate transaction prices in January, it validated the tightening signal and ignited the rally. Every major PrNd price spike of the past decade has started with a Chinese quota or concentrate price move.

02Electric vehicle traction motor demand

Global passenger EV sales are forecast to reach 22.9 million units in 2026 — a 6.6% year-on-year increase (BMI). The dominant motor technology remains the interior permanent magnet motor, which uses 1–3 kg of NdFeB per vehicle. BMI expects global NdPr oxide demand to increase by 7.7% year-on-year in 2026 as a direct result. While rare earth-free motor alternatives are gaining R&D attention, permanent magnet motors are expected to remain the dominant EV drivetrain technology through at least 2030 due to superior efficiency and power density.

03Offshore wind turbine build-out

BMI forecasts global offshore wind capacity to grow 14.3% to 109.1 GW in 2026. Offshore turbines disproportionately favour direct-drive permanent magnet generators, which require significantly more NdPr per megawatt than geared designs. As offshore wind expands beyond its traditional European strongholds into developed Asian markets, magnet demand per unit of new capacity installed remains high. Wind and EV together account for the large majority of incremental PrNd demand growth, and neither sector is slowing.

04Structural supply deficit — second consecutive year

Despite NdPr oxide production rising approximately 7.4% year-on-year in 2026 (driven primarily by China, with contributions from MP Materials and Australian ramp-ups), BMI forecasts the NdPr market will remain in supply deficit for the second consecutive year. Demand is growing faster than new separation capacity can come online. Non-Chinese supply projects are ramping, but building a full rare earth separation and magnet production chain is a multi-year effort. China still controls roughly 85% of global refining capacity.

05Export policy uncertainty and precautionary buying

China suspended its October 2025 rare earth export controls for one year as part of a broader US–China trade détente. That pause expires in November 2026. As the deadline approaches, Western OEMs and magnet buyers are expected to engage in precautionary stockbuilding — the same dynamic that amplified the January–April rally. The suspension reduced near-term supply shock risk, but it did not resolve the structural concentration issue: China holds the processing bottleneck and can activate export controls again.

What It Means for Your Cost: The Gap Between Benchmark and Invoice

The SMM NdPr oxide benchmark is the industry’s reference price — but it is a Chinese domestic, ex-VAT, delivered-to-works figure for large-volume industrial transactions. As a European or North American buyer of finished magnets, the number on your invoice is meaningfully higher.

The gap builds up in layers: the oxide-to-metal conversion adds roughly 10–20%; export levies, freight, and applicable duties add further; and outside the integrated Chinese supply chain, spot market quotes carry an additional premium reflecting smaller volumes and a less liquid market. In practice, when the SMM benchmark reads $90/kg, a Western buyer’s landed cost for the refined NdPr content in their magnets is typically in the $115–$130/kg range — before the magnet maker’s processing margin and profit.

A useful policy anchor: the US Department of Defense-backed offtake agreement with MP Materials sets a floor of approximately $110/kg NdPr — representing what a Western, fully-integrated rare earth supply chain is expected to cost at industrial scale. Buyers sourcing outside the Chinese system should treat this as a reference floor, not a ceiling.

The practical rule: Always translate the SMM benchmark to your actual landed cost before making procurement decisions. The two numbers differ by 30–50% in a normal market — and more during periods of tight ex-China availability.

What Comes Next: Q3–Q4 2026 Outlook

The June pullback has brought NdPr oxide back toward a level more consistent with near-term fundamentals — but it has not resolved the structural supply deficit. Three scenarios frame what H2 could look like, each with different implications for when and how much to order:

Stabilisation in this range through Q3 is the analyst consensus, absent a fresh demand catalyst or supply disruption. The structural deficit supports a floor; speculative excess has been unwound.

November truce expiry triggers precautionary buying; MIIT quota disappoints; or a major Western OEM accelerates EV ramp. Any of these could retest the April highs.

A sharp Chinese quota increase or significant EV demand miss. Neither is the current consensus — a return to 2025 lows would require both simultaneously.

The key near-term event is the November 2026 expiry of China’s one-year export control truce. As that date approaches, Western buyers are expected to begin restocking ahead of potential new restrictions — which could push prices back toward the upside scenario before year-end, regardless of whether actual controls are reimposed. A return to sub-$60/kg would require both a significant Chinese quota increase and a major EV demand miss simultaneously — not the current consensus. The base case points to gradual stabilisation in the $85–$100/kg range, but with asymmetric upside risk in Q3.

For buyers, this shapes the timing question directly: the June correction has opened a window, but the November deadline means that window is unlikely to stay open past Q3. Confirming H2 allocation and reviewing grade-level cost exposure now costs nothing; waiting until prices move again costs significantly more.

What It Means for Your Next Order: Involve Your Supplier Now

Magnet capacity gets allocated to known customers first. A supplier who understands your grade, volume, and schedule can offer quarterly price adjustment mechanisms tied to the SMM benchmark, advise on grade substitution that reduces HREE exposure, and flag allocation constraints before they become delivery problems. At XHMAG (昕徽磁业), we work with motor, sensor, and power-tool manufacturers across Europe and North America on exactly this kind of procurement planning — not just on quoting. In a market shaped by quota cycles and policy expiry dates, that relationship is more valuable than ever.Contact us:tony@xh-magnet.com

Frequently asked questions

What does PrNd mean, and is it the same as NdPr or PRND?

PrNd, NdPr, and PRND all refer to the same blended oxide of praseodymium and neodymium — the primary rare earth input for sintered NdFeB permanent magnets. The order of the letters is stylistic; the material is identical. In magnet industry usage, NdPr oxide (SMM code SMM-RE-OX-001) is the standard benchmark reference.

How much does the PrNd price affect what I pay for finished NdFeB magnets?

PrNd accounts for roughly 50–65% of a finished NdFeB magnet’s raw material cost, depending on grade. A doubling of PrNd oxide price (as happened in 2026 Q1) typically translates to a 25–40% increase in finished magnet cost, modulated by grade, coating, tolerance, and the supplier’s hedging position.

Will PrNd prices fall significantly in H2 2026?

The current analyst consensus does not forecast a return to 2025 price levels within 12 months. The structural deficit is expected to persist through at least 2026, and the November export control truce expiry introduces upside rather than downside risk for Q3–Q4. A stabilisation range of $85–$100/kg oxide is the base case for Q3.

How can I protect my procurement budget against rare earth price swings?

The most effective levers: (1) quarterly price adjustment clauses indexed to the SMM NdPr benchmark; (2) buffer stock on high-run-rate grades during corrections like the current one; (3) grade substitution evaluation — lower-Dy versions may meet your thermal spec; (4) dual-sourcing with at least one supplier who can confirm Western supply chain traceability.

The bottom line

Two questions drove this guide. What’s driving rare earth costs in 2026? Five structural forces — Chinese quota tightening, EV demand growth, offshore wind expansion, a second consecutive supply deficit, and export policy uncertainty — pushed PrNd oxide from $53/kg to $138/kg before a partial correction brought it back to $90/kg. None of those forces have been resolved; they define the market environment for the rest of the year.

What does it mean for your next order? It means the June pullback is a window, not a trend reversal. Prices are 70% above the year-open, the November truce expiry introduces Q3 upside risk, and supply chain capacity gets allocated to existing relationships before the spot market. Locking in H2 allocation, understanding your grade-level cost exposure, and engaging your supplier now are the practical responses — not waiting for a return to 2025 levels that the current consensus does not support.